Financial freedom is not about hoarding wealth.

It is about building it intelligently — and protecting it from unnecessary erosion.

Efficient investing is the discipline that turns savings into lifetime independence.

But efficiency is not automatic.

It requires structure, transparency, and oversight.

The Mathematics Of Compounding (And Why Small Mistakes Matter)

Compounding is powerful.

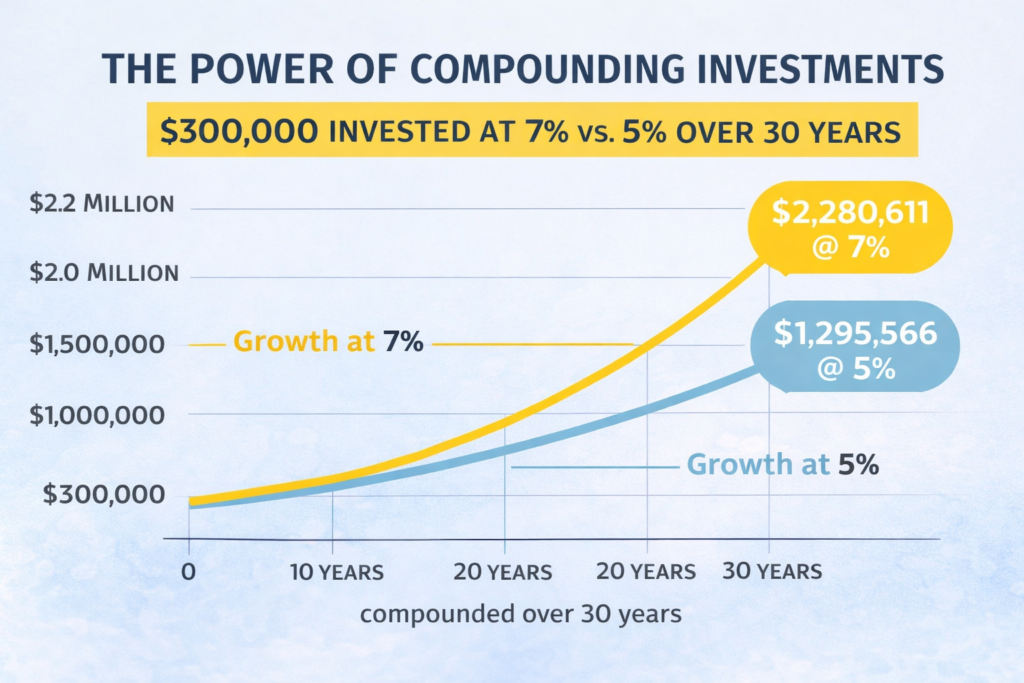

A $300,000 portfolio earning 7% annually grows to approximately $2.2 million in 30 years.

At 5%, that same portfolio grows to roughly $1.3 million.

That 2% difference may come from:

Over decades, small inefficiencies compound into massive lost opportunity.

The difference is not theoretical.

It is life-changing.

A $300,000 investment earning 7% annually grows to over $2.28 million in 30 years, while the same portfolio earning 5% reaches approximately $1.29 million — illustrating how small differences in return compound dramatically over time.

Assumes annual compounding, no additional contributions, no withdrawals, no taxes.

Efficient Investing Requires:

Every investor should understand:

What do I own?

Why do I own it?

How much am I paying?

What are the risks?

If those answers are unclear, efficiency may already be compromised.

The Silent Wealth Killers

Most investors do not lose wealth in dramatic collapses.

They lose it gradually through:

Underperformance compounds.

So do conflicts.

Growth Phase Vs. Protection Phase

Efficient investing evolves.

In your 30s and 40s:

Growth dominates.

In your 50s:

Balance matters.

In retirement:

Preservation and controlled distribution become critical.

A static strategy across decades is rarely efficient.

Trust Is Important. Verification Is Essential.

Many investors assume:

“If my account went up, everything must be fine.”

Not necessarily.

Material underperformance, excessive fees, unsuitable risk exposure, or undisclosed conflicts may exist even in a positive-return year.

You deserve transparency.

You deserve alignment.

You deserve a strategy built for you — not for someone else’s commission structure.

When Efficiency Breaks Down

If you suspect:

It may not simply be inefficiency.

It may be misconduct.

And that distinction matters.

The Difference Between Efficient Investing And Investment Fraud

Efficient investing builds wealth.

Fraud, misconduct, and conflicts quietly erode it.

If you are unsure whether your portfolio inefficiency is simply poor strategy — or something more serious — it is worth a careful review.

Schedule a Confidential Portfolio Review

Speak With An Investment Fraud Attorney

If you believe your portfolio suffered from:

You may have options.

A disciplined review of your account documents can often reveal what went wrong.

Financial freedom should not be undermined by misconduct.

Frequently Asked Questions

How Much Do Fees Impact Long-Term Wealth?

Even a 1% annual fee difference can reduce long-term portfolio value by hundreds of thousands over 25–30 years.

Fees compound negatively.

What Is A Suitable Investment?

A suitable investment aligns with your age, risk tolerance, objectives, liquidity needs, and financial profile.

Anything misaligned may create legal exposure for the recommending advisor.

Can You Recover Losses Caused By Unsuitable Investments?

In some cases, yes.

Investors may have claims through FINRA arbitration or litigation depending on the circumstances.

Each case requires careful analysis.

How Often Should A Portfolio Be Reviewed?

At minimum annually — and whenever there is a life event such as retirement, inheritance, divorce, or major market change.